The Buzz on Paul B Insurance

Table of ContentsPaul B Insurance for BeginnersNot known Details About Paul B Insurance Our Paul B Insurance IdeasNot known Details About Paul B Insurance The 7-Second Trick For Paul B Insurance

The idea is that the cash paid in cases over time will be less than the overall premiums accumulated. You may feel like you're throwing cash out the window if you never sue, yet having piece of mind that you're covered in the occasion that you do experience a substantial loss, can be worth its weight in gold.Picture you pay $500 a year to guarantee your $200,000 home. You have one decade of making settlements, as well as you've made no cases. That comes out to $500 times 10 years. This indicates you've paid $5,000 for residence insurance policy. You start to ask yourself why you are paying a lot for nothing.

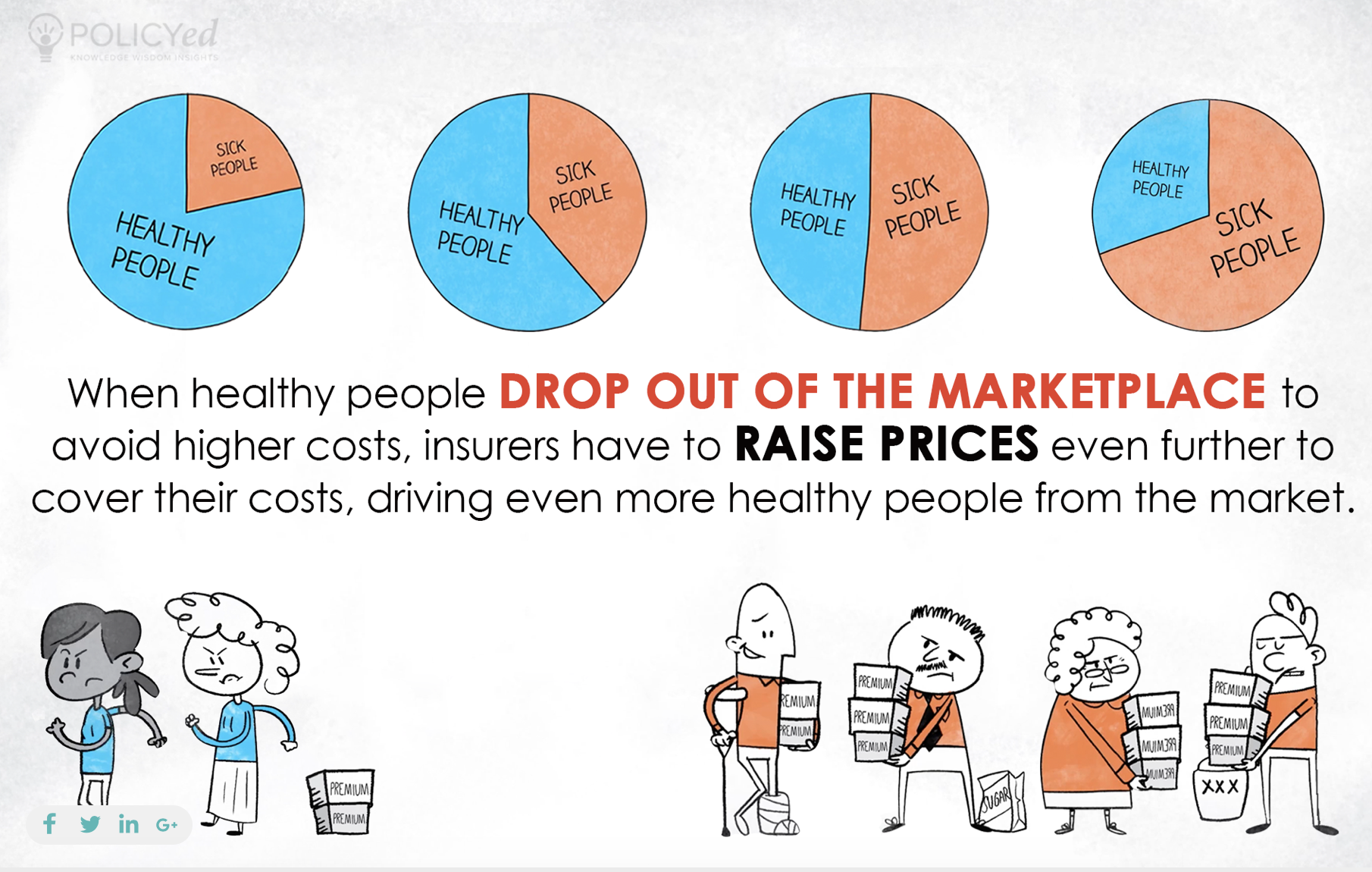

Since insurance is based upon spreading out the risk amongst lots of people, it is the pooled cash of all individuals paying for it that permits the firm to develop possessions and cover claims when they happen. Insurance is a business. It would certainly be wonderful for the companies to simply leave prices at the same degree all the time, the reality is that they have to make adequate cash to cover all the potential insurance claims their insurance holders may make.

A Biased View of Paul B Insurance

just how much they entered premiums, they have to revise their rates to make cash. Underwriting changes and also rate increases or decreases are based upon results the insurance business had in past years. Depending upon what business you buy it from, you might be dealing with a captive representative. They sell insurance coverage from only one company.

The frontline individuals you deal with when you purchase your insurance policy are the agents and brokers that stand for the insurance firm. They an acquainted with that business's products or offerings, but can not talk towards other firms' plans, pricing, or product offerings.

Top Guidelines Of Paul B Insurance

The insurance policy you require varies based upon where you go to in your life, what type of properties you have, and what your long-term objectives and also tasks are. That's why it is important to make the effort to discuss what you want out of your policy with your representative.

If you obtain a car loan to purchase a cars and truck, as well as then something happens to the automobile, space insurance will certainly repay any type of part of your finance that common vehicle insurance policy does not cover. Some lenders require their debtors to lug void insurance coverage.

Paul B Insurance Can Be Fun For Anyone

Life insurance coverage covers the life of the guaranteed person. Term life insurance covers you for a duration of time selected at purchase, such as 10, 20 or 30 years.

Term life is preferred because it provides big payouts at a lower expense than long-term life. There are some variants of regular term life insurance policy policies.

Permanent life insurance coverage click here to read policies build cash value as they age. A portion of the premium repayments is contributed to the cash value, which can earn interest. The cash worth of whole life insurance policies expands at a set price, while the money worth within universal policies can Continued fluctuate. You can use the cash worth of your life insurance policy while you're still active.

The Basic Principles Of Paul B Insurance

If you compare ordinary life insurance policy rates, you can see the distinction. $500,000 of whole life protection for a healthy 30-year-old lady prices around $4,015 yearly, on standard. That same degree of coverage with a 20-year term life policy would certainly cost approximately about $188 every year, according to Quotacy, a broker agent firm.

Those financial investments come with even more danger. Variable life is another long-term life insurance alternative. It seems a whole lot like variable universal life however is in fact different. It's a different to whole life with a fixed payment. Insurance holders can use investment subaccounts to expand the cash money value of the policy.

Here are some life insurance basics to help you better understand how coverage works. For term life plans, these cover the price of your insurance policy as well as management expenses.